How can you tell if a mandated curriculum is truly there for your benefit or as part of a political agenda? Since the implementation of the Ramsey Education Foundations in Personal Finance curriculum to fulfill the state mandated personal finance graduation requirement, there has been controversy surrounding its utility in the everyday student’s life and the intentions behind it. The curriculum is part of Ramsey Solutions, a company which provides financial guidance started by Dave Ramsey, a radio talk show host and entrepreneur.

Alison Hollis, an AP Literature and Composition teacher, was shocked that Dave Ramsey’s financial philosophies made it into a mandated public school curriculum, because to her, it is highly connected to a conservative Christian belief system.

“So on the surface, I think Ramsey’s philosophies make a lot of sense, right?” Hollis said. “It’s all about your personal decisions … There is some judgment that comes with his resources when it comes to debt. There is a lot of connection between debt and sinfulness. And I know this because my college roommate’s parents are really good friends with him and went to his church.”

Another point Hollis and some students like Eric Liu (12), who is taking the course online, have is that the course ignores systemic challenges, which can deeply affect a person’s financial situation despite their best efforts. This makes some students feel that parts of the curriculum cannot be applied to their situation.

“But I think part of his philosophy ignores some systemic challenges,” Hollis said. “Also, a lot of his philosophies require — sometimes when you look at it — [that] you just need to make more money and that’s not necessarily fully in that person’s control. I’m a teacher. I can’t just make more money as a teacher. I just have to keep teaching. And then I might [get] more degrees, but there’s nothing that I can do this week or next week to increase my salary as a teacher … that’s not within my locus of control.”

The course is centered around five main ideas or what it calls the “5 Foundations” which are to save a $500 emergency fund, get out and stay out of debt, pay for your car and for college in cash, and build wealth and give charity. However, many like Liu feel this is unrealistic and ignores larger issues.

“The third and fourth [points] are especially ridiculous, especially in this economy … The third point demands you to pay for college and your car in cash,” Liu said. “No one has that kind of money these days … Yes, financially, it makes the most sense because you’re not taking out a loan or anything, but it’s just not something that most people can afford unless you already have tons and tons of money. This isn’t personal finance. It’s not teaching you how to do personal finance. This is for telling rich people how to keep being rich. And not only that, it also puts all the problems of the economy onto the individual.”

Others argue that the course is realistic, that it is indeed possible to pay for college with cash. Amy Thornton is one of the personal finance teachers and has both in-person and online classes.

“I think [the course is] realistic if you are willing to sacrifice some things,” Thornton said. “Now, nothing is ever going to be realistic if you aren’t willing to sacrifice. I know that you can pay cash for college. I did it. My daughter did it.”

Besides being concerned about paying cash for what are usually some of teen life’s biggest investments like college and a car, some believe there are lessons that would have been more useful because they address situations students will likely encounter.

“I feel like something that would have benefited me, especially because this is meant for high school students … [is] a clear guide on completing the FAFSA or any other government aid programs that can help you in paying off colleges or paying off a house, paying off cars,” Liu said. “It can help you explain the long term of taking on loans and it can explain how loans will be necessary for most people. So rather than saying … ‘don’t have loans,’ it’s explaining how to take loans with minimal debt. That will be a lot more useful, because this is something that most people can apply to their lives.”

Thornton, who has been teaching the curriculum since it was first mandated three to four years ago, says the course is realistic despite objections from several teachers and students who believe that Ramsey’s background as a millionaire disqualifies him from giving such advice and marketing it to the average person. She says that Dave Ramsey was from a middle class family and made his money himself, and learned how to manage it after going bankrupt.

“I’ve had some teachers go, ‘it’s not realistic … and … it’s realistic,’” Thornton said. “I think … society has taught us that the norm is that you have to take out a student loan to go to college — that you have to have debt. In 2020, the average household debt in America was $13,000, and so that has become the norm. And so anytime somebody says you don’t have to have debt, you can do it with cash and things. I think people go, ‘Oh no, there’s no way,’ because the norm is saying the only way to do it is through debt.”

While many students taking the online course feel it is not realistic and thus not helpful, many in-person students say the class has strengthened their finance management and organization and made them feel more prepared. Julia Mendez (10) is currently taking Thornton’s class in-person.

“Mostly I think why [the experience is] so different from online and in person is because Ms. Thornton will skip certain parts of the video and she will pause certain parts of the video to talk about her personal experience as a teacher … but there were definitely things in the video I was like, ‘I’m sure that’s easy to say when you’re like a millionaire,’” Mendez said. “And it’s just like, when you just get up and you do it again and you work hard and then you’re there, that type of stuff definitely feels kind of out of touch. But most of the things that she shows us are things that help you as a person manage your money regardless of situation. It’s not so much as how to make more money as it is how to manage the money you have.”

( ZAHRA ALTAREB//THE SCROLL)

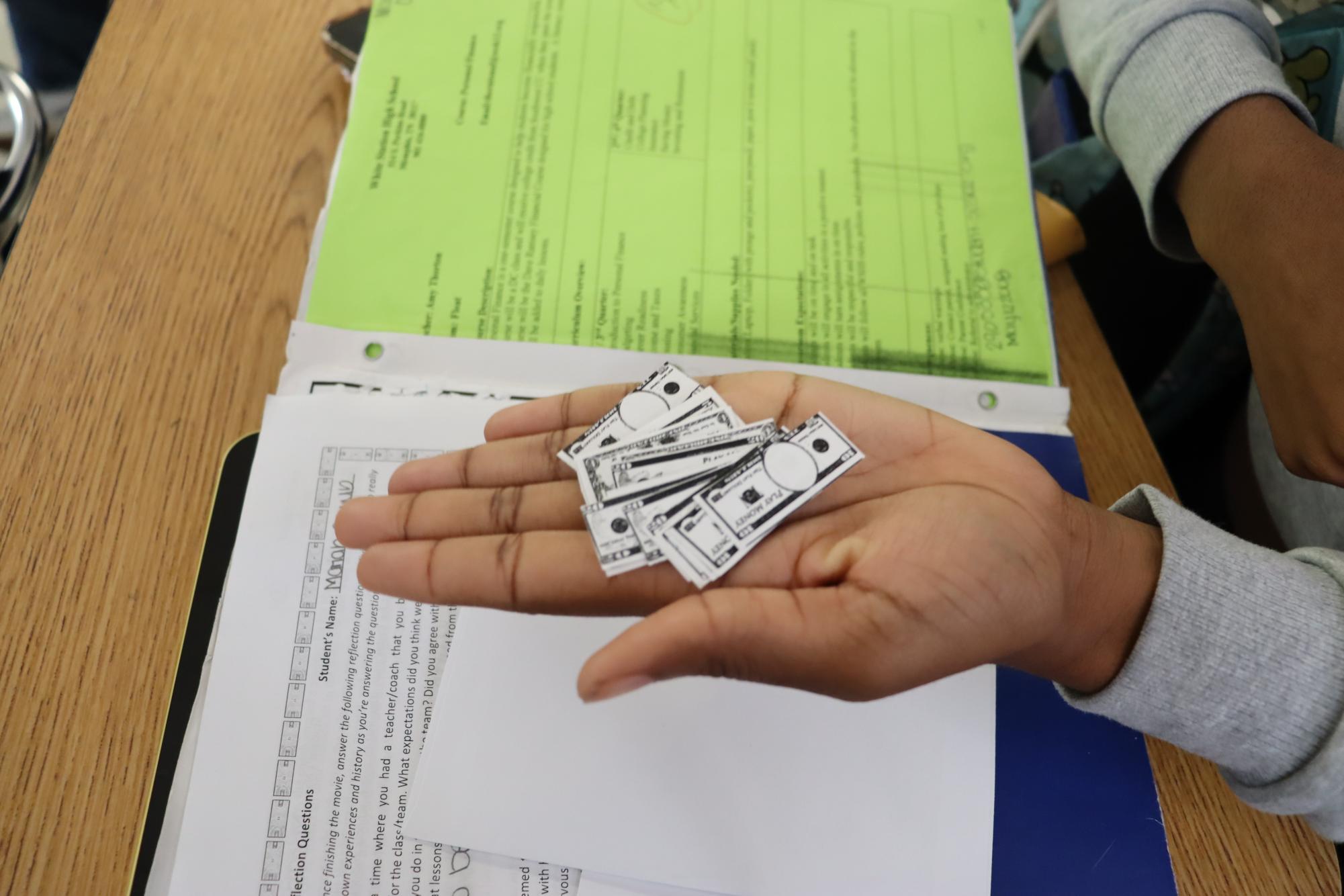

But all of this brings into question the true benefit of the Ramsey curriculum if, as Mendez says, that teachers so drastically change the material and the experience of taking the class. This has a significant impact on students’ quality of learning.

“I think [the curriculum] is a solid base, a foundation, but I think without the class aspect, the interaction, the discussion, and the anecdotes that Ms.Thornton adds … it won’t be as helpful because you don’t get the experience of Ms.Thornton as the class, which is she has her own money system,” Mendez said. “She gives everybody in the class a certain amount of money each month under their own salary and each month you are required to make a budget.”

One thing that almost many agree on however, is the importance of financial knowledge and financial responsibility for the stability of everyone. In Hollis’s opinion, a lack of financial responsibility and knowledge is what led to the 2008 financial crisis.

“I graduated from college during the financial collapse. I’ve seen what a system looks like when we are not being fiscally responsible,” Hollis said. “And I very much understand the big lasting impacts of when a huge group of people from top of the system all the way to the bottom of the system are not being financially responsible … I know what happens. I’ve seen it and experienced it and lived through the consequences of it so I think it’s very important [to have personal finance as a graduation requirement].”

Despite the objections some may have to the curriculum, it is important to Thornton that her students are able to learn how to be in control of their lives through learning how to control their money.

“What I hope [my students] benefit the most … is that they get a sense that they can budget and that they have control of their money, and they don’t have to go into debt to have a good life,” Thornton said. “I want them to … feel like they have power over their money and that they’re going to make their money work for them.”